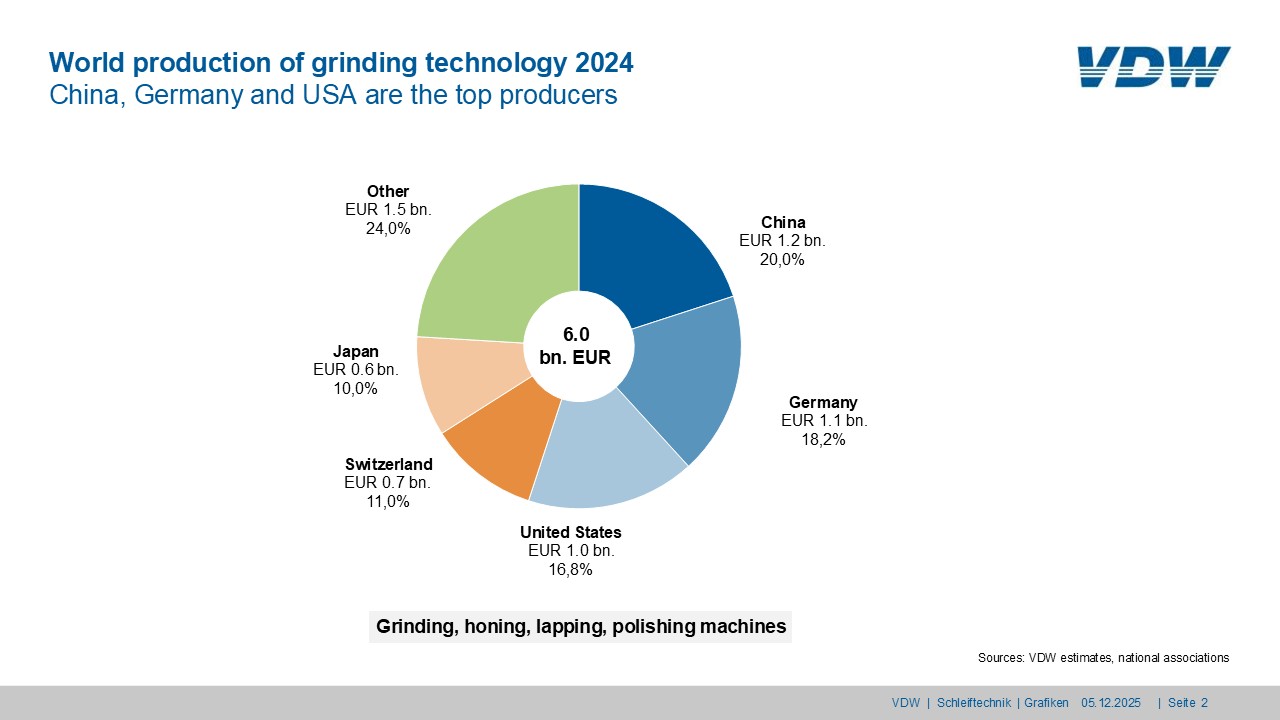

Between downturn and glimmer of hope

Decline in production

In the first half of 2025, production of grinding technology fell by 15 percent compared to the previous year – from €501 million to €425 million. Particularly serious: Exports slumped by almost a quarter, from €398 million to €306 million. While exports are weakening, technology projects are supporting domestic sales. Domestic demand is increasingly being met by domestic suppliers. Domestic consumption stagnated at €247 million, increasing by only 1 percent. Overall, trade intensity is declining: fewer exports, fewer imports.

Strong first quarter for orders

There was a glimmer of hope at the beginning of the year: In the first quarter, incoming orders rose by an impressive 85 percent compared to the previous year. The driving force was foreign countries, with an extraordinary increase of 120 percent. Together with the following two quarters, foreign sales rose by 17 percent, pushing up the overall average, while domestic sales weakened significantly, falling by 24 percent in the same period – a reversal of the trend seen in 2024. The eurozone performed particularly well, with growth of around one-third. Over the first nine months, there remains a slight increase of 4 percent overall. "The first quarter was a real ray of hope. However, weak domestic orders show that recovery is anything but certain," emphasizes Bernhard Geis, Head of Economics and Statistics at VDW.

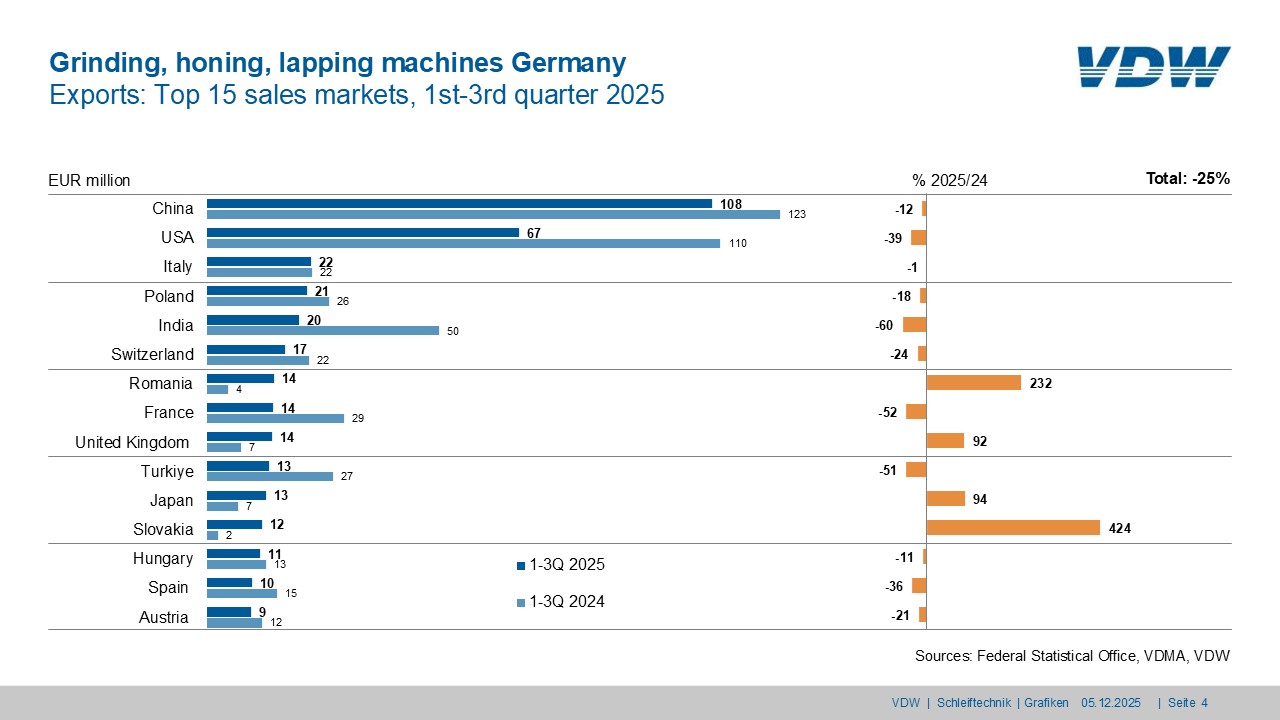

Export markets: China out front, USA weakening

Exports of grinding, honing, lapping, and polishing machines fell by a quarter overall in the first three quarters of 2025. China remains the most important trading partner with around €108 million, despite a decline of 12 percent. The USA recorded an above-average decline of 39 percent, presumably influenced by tariff policy. Italy (€22 million) and Poland (€21 million) are almost neck and neck in third and fourth place. India is experiencing a particularly sharp decline of 60 percent, which could indicate consolidation after years of growth. Markets in the Middle East (up 59 percent) and Southeast Asia (up 115 percent) offer hope, although their share of total exports remains low at around 3 percent and just under 2 percent, respectively.

Switzerland continues to dominate imports

Switzerland remains the undisputed leader in imports, with a share of 42 percent. Czechia follows, but with an above-average decline of 22 percent. China remains relatively stable with a slight decline of 2 percent.

Volatile markets demand greater flexibility and stronger diversification

Grinding technology will be under considerable pressure in 2025. Production and exports are declining significantly, while domestic consumption currently remains stable. The positive development in foreign orders – especially from the eurozone –underscores the importance of international markets despite declining trade intensity. Bernhard Geis sums it up: "The industry needs to realign itself strategically: Greater flexibility and stronger diversification of sales markets are more crucial than ever in order to position companies competitively in the long term."

Our economy trend is also available for download: Download press release (PDF, 194 KB)

zurück zur Übersicht

")